To meet its net-zero targets, the UK needs a transition to cleaner energy and greener transport. This will require larger and more stable supplies of critical minerals. The government should also implement policies to improve mining practices, reduce demand, and increase reuse and recycling.

The UK government launched its review of net zero in September 2022. This asks how to ensure that the country delivers its commitment for there to be net-zero carbon emissions by 2050, while at the same time seizing the benefits from future innovation and technologies.

It is now an open secret that the global economy will require an increasing quantity of raw materials to achieve the 'green transition'. To reach net zero, governments need to develop a responsible and sustainable supply of these energy transition minerals that are required for renewable energy sources and to produce low-carbon alternative transport options, such as electric vehicles.

The UK’s net-zero review and critical minerals strategy provide a huge opportunity to launch the UK economy into a cleaner and more secure future if the possibility of acute shortages of key metals and minerals is addressed in time.

The energy crisis that has emerged as a result of the war in Ukraine has led to policy U-turns back towards fossil fuels across Europe, with countries scrambling to develop new sources of natural gas supply at breakneck speed. UK investments in further North Sea oil and gas exploration are being touted as a strategic imperative, and fracking was recently being openly considered by the government – a position that was unimaginable a year ago during COP26.

The experience of the policy reversal that has brought the once unimaginable spectre of new hydrocarbon investments back to the fore offers critical lessons on how not to approach the sourcing of energy transition minerals in the years ahead.

What are energy transition minerals and why do they matter?

While recent newspaper headlines have been dominated by discussions of the supply of natural gas, mined raw materials are becoming increasingly important for large Western economies.

The transition to a net-zero economy and the subsequent appetite for electric vehicles, wind turbines, solar panels and new electricity connections will require huge quantities of energy transition minerals (International Energy Agency, IEA, 2021; World Bank, 2017). These include copper, nickel, aluminium, cobalt and lithium, as well as the ‘rare earth’ elements neodymium, praseodymium and dysprosium (see Figure 1).

Figure 1: Materials critical for transition to a low-carbon economy, by technology type

Source: McKinsey & Company, 2022

This demand for minerals is mostly driven by the significantly higher material intensity of renewable energy technologies compared with fossil fuel-based power generation and transport (Hund et al, 2020).

In a 2021 report, the IEA finds that the production of an electric vehicle needs approximately six times more minerals than a conventional car (IEA, 2021). Offshore wind technology requires 12 times more metals and minerals for every megawatt (MW) of electricity it produces compared with producing the equivalent amount of electricity with natural gas (see Figure 2).

It is important to note that despite the large material footprint of producing an electric vehicle – which is primarily driven by the energy and resource intensity of the mining, smelting and fabrication processes – their lifecycle carbon emissions are 62% lower than petrol cars (Bieker, 2021).

Similarly, electricity generated by offshore wind produces 95% fewer carbon emissions than the equivalent electricity production with natural gas (Thomson and Harrison, 2015).

Figure 2: Material intensity of energy and transport technologies

Source: IEA, 2021

Further, the World Bank finds that extraction of energy transition minerals will need to increase five-fold by 2050 to meet demand for clean energy technologies (World Bank, 2017). This translates to more than three billion tonnes of minerals and metals that will be needed for wind, solar and geothermal power, as well as energy storage.

Electric vehicle production is responsible for 50-60% of the demand for energy transition metals, followed by electricity networks and solar photovoltaics (35-45%), and then other technologies (5%) (KU Leuven, 2022).

Given the large increase in demand, it is paramount to expand the collection and recycling rates of metals when products in which they are used reach the end of their life/use. The European Commission and KU Leuven University find that even with steadily increasing collection and recycling rates, only a fraction of the rapidly rising demand can be met by recycling efforts (Blagoeva et al, 2016; KU Leuven, 2022).

Mature recycling industries for materials such as copper, steel and aluminium currently reach end-of-life recycling rates of between 30% and 60%. But for several very important energy transition minerals, such as lithium and rare earth elements, the rate is less than 1% (KU Leuven, 2022).

A large increase in production from primary sources will therefore be necessary for the foreseeable future. Indeed, the start of new mining projects from untapped resources will be required at a scale not seen before.

What is the UK government doing about this?

Even though these challenges have been known for years, most Western governments have been slow to act. The UK only published its first critical minerals strategy in July 2022.

The publication sets out a ten-point vision for ensuring the resilience of supply chains for critical minerals – defined as minerals with high economic vulnerability and high global supply risks. The strategy covers a wide breadth of interventions and focuses on three areas of intervention:

- Accelerating the UK’s domestic capabilities.

- Collaborating with international partners.

- Enhancing international markets.

The UK follows other Western countries, such as Australia, Canada, members of the European Union (EU) and the United States, which have all established similar strategies.

The strategy is also significant as it is the first time that the government has acknowledged that the UK and Europe have become vulnerable to supply chain disruptions and shortages of vital metals and input materials. This has occurred as greater raw material production and refining capacities have been offshored over recent decades.

Since the 1970s, global metal extraction has more than tripled, reaching 1.2 tonnes per capita in 2017. The European continent contains less than 7% of the global population, but uses around 30% of all metals extracted globally (European Environmental Bureau, 2021).

In particular, there is a disproportionate reliance on China, which is the largest primary supplier of refined metals to Europe. China processes 40% of global copper, 35% of nickel, 65% of cobalt, 87% of rare earth oxides and 58% of lithium (Mining Technology, 2022).

While subsequent UK governments have actively promoted renewable energy and electric transport – by subsidising and promoting green manufacturing activities, including battery cell production and user uptake of new technologies through electric vehicle subsidies – greater attention should be paid to sourcing the raw input materials for these products made and bought in the UK.

As a result, the critical minerals strategy is certainly a welcome sign. It acknowledges that supplying enough raw materials to allow the global economy to make the transition to net zero within the timeframe required by the Paris Agreement will require government intervention and support for upstream raw material production (House of Commons, 2010).

What are some of the criticisms of the UK’s critical minerals strategy?

First, despite the rhetoric of the strategy (highlighted by the ministerial foreword), the choice of minerals determined to be highly critical for the UK does not align with net-zero priorities.

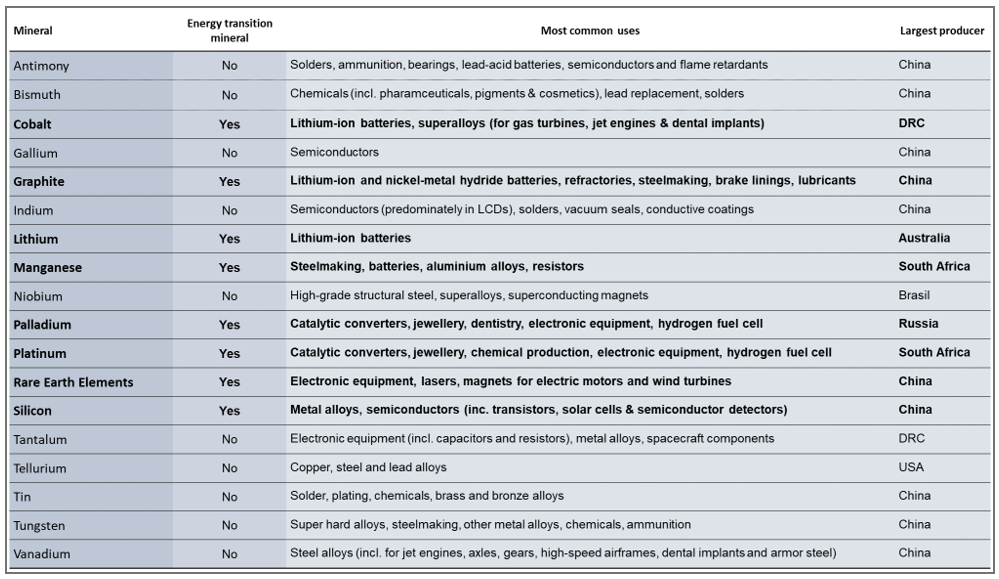

Only eight of the 18 minerals on the list are classed as energy transition minerals by the most reputable studies (IEA, 2021; IRENA, 2021; KU Leuven, 2022). The majority are more important for defence, and advanced information and communication technologies (ICT) applications (see Table 1).

Contrary to the ministerial narrative, the strategy appears to be primarily driven by a strong geostrategic focus on ensuring access to critical inputs for technologies imperative to the UK’s national security interests, while reducing reliance on China and other authoritarian states, a strategy increasingly touted as ‘friend-shoring’ (Bloomberg, 2022).

Working with friendly suppliers could provide more certainty in some instances. But basing the strategy on geopolitical goals rather than the realities of global mineral supply chains runs the considerable risk of developing a strategy that fails to deliver the ultimate goal of responsibly sourcing sufficient supply of the raw materials needed for the energy transition.

Table 1: Minerals listed in the critical minerals strategy, their uses and the world’s largest producer

Sources: IEA, 2021; IRENA, 2021; KU Leuven, 2022; UK Government, 2022; United States Geological Survey, 2022

Second, the strategy pledges to ‘champion London as the world’s capital of responsible finance for critical minerals’ and ‘support UK companies to participate overseas in diversified responsible and transparent supply chains’. Yet the government has pledged no funding for either domestic or international development of critical mineral primary supplies. This sets it apart significantly from its peers.

The EU pledged €2 billion for the development of critical mineral supplies in its European Critical Raw Materials Fund. Canada pledged CAN $3.8 billion in the 2022 budget and Australia committed AUS $2 billion through its Critical Minerals Facility.

The United States has invested more than US $1 billion in domestic critical mineral projects and pledged billions of dollars more as part of a recent infrastructure bill. The US government’s critical minerals support scheme is even more openly aimed at securing critical supplies for its defence industry and making itself less reliant on raw material imports from China than the UK’s strategy.

Third, the inclusion of the need to increase recycling and reuse interventions to reduce pressures on primary supply in the strategy is welcome. This includes an explicit aim of developing a circular economy for metals and minerals in the UK.

But the strategy fails to explore potential demand-side measures that could reduce the large supply-side pressures, such as reducing energy demand from housing, transport and manufacturing.

Last, it is a positive sign that the importance of environmental, social and corporate governance (ESG) measures is highlighted explicitly in the strategy, as the sustainability of future mining operations needs to improve.

Averting the climate crisis cannot come at the environmental and social costs that mining is still widely associated with, such as deforestation, negative impacts on biodiversity and freshwater, large greenhouse gas emissions, air pollution and negative consequences for indigenous people (Lèbre et al, 2020; Tost et al, 2018; Watari et al, 2020).

What actions should we expect policy-makers to take now?

The long-held laissez-faire approach of the UK government has operated on the premise that international commodity markets would provide the primary supply of critical metals for UK manufacturing. This will only hold up in the environment of an accelerated energy transition and its material demands if four key policy areas are addressed.

Policies that follow the critical minerals strategy need to go beyond the purely geostrategic interests of securing raw materials

Given the specific constraints and requirements of energy transition minerals, policy-makers will have to develop a stand-alone policy position and interventions. Combining the issues of sourcing raw materials that are primarily of interest for the defence and ICT industry and the sourcing of energy transition minerals is problematic. This approach will hinder the development of fit-for-purpose schemes to improve the availability of responsibly sourced energy transition minerals at the required quantity and price.

Sustainability and the promotion of sustainable extraction methods have to be at the core of any future government support

Mining is a traditional industry, and mineral extraction processes have changed little in past decades, as mining companies carry out significantly less research and development (R&D) relative to other industries (Bartos, 2007; Sánchez and Hartlieb, 2020).

It is, therefore, important that the government explores options to promote investment in innovation activities to develop more sustainable raw material extraction methods and better integrated mine planning.

It will also need regulations and support programmes that lower the cost of capital for more sustainable mining operators to ensure a just transition for mining communities, and the mitigation of negative externalities from mining operations.

Many of the biggest customers for energy transition minerals are already more insistent on higher sustainability than other mineral users. By being an early mover in financing cutting-edge sustainable extraction technologies and best-in-class mining operations, the UK can develop a significant competitive advantage over other research and financing hubs.

This is as much about demand as it as a supply-side story

Demand for energy transition minerals will necessarily increase. But it should be a prerogative for the UK government at least to highlight and explore the potential of demand reduction interventions, such as the promotion of car sharing, improved public transport networks and increasing the energy efficiency of the UK housing stock. Ultimately, more efficient use of energy and greater material efficiency goes hand in hand with lower material demand.

An action roadmap needs to be published as soon as possible

Apart from the creation of the Critical Minerals Intelligence Centre, limited concrete actions have been announced alongside the publication of the strategy. Therefore, it is important that the strategy is translated into an actionable roadmap as fast as possible.

Conclusion

Moving swiftly towards renewable energy is a necessary step to addressing the long-term challenges posed by climate change, as well as the current cost of living and energy crises. But it is vital that this happens alongside steps to protect the country from a critical minerals crisis in future. Done right, this will also contribute much-needed opportunities for the UK economy, and ensure the country’s energy security.

Where can I find out more?

- Review of net zero: UK government report.

- UK critical minerals strategy: UK government.

- Critical minerals: International Energy Agency.

- Climate-smart mining: World Bank Group.

- Metals for clean energy: KU Leuven report.

- Critical raw materials: British Geological Survey.

- Technology metals for a green future: University of Exeter MOOC.

Who are experts on this question?

- Paul Lusty – British Geological Survey

- Frances Wall – Camborne School of Mines, University of Exeter

- Paul Ekins – University College London